Today, we're going to take a closer look at something that may seem quite ordinary: homeowner's insurance policies. But as you'll soon see, these documents are far from ordinary, and they contain some intriguing clues about what might be happening behind the scenes. The conspiracy minded might be forced to conclude that there is an insurance conspiracy.

Changes in Homeowner's Insurance Policies

One of my close friends is currently renewing her homeowner's insurance policy. As we reviewed the document together, one thing caught our attention: a series of exclusions that were not present in her previous policy. These exclusions are significant because they suggest that there could be potential events or circumstances that might not be covered by standard insurance policies.

To give you an idea, here is a brief overview:

-

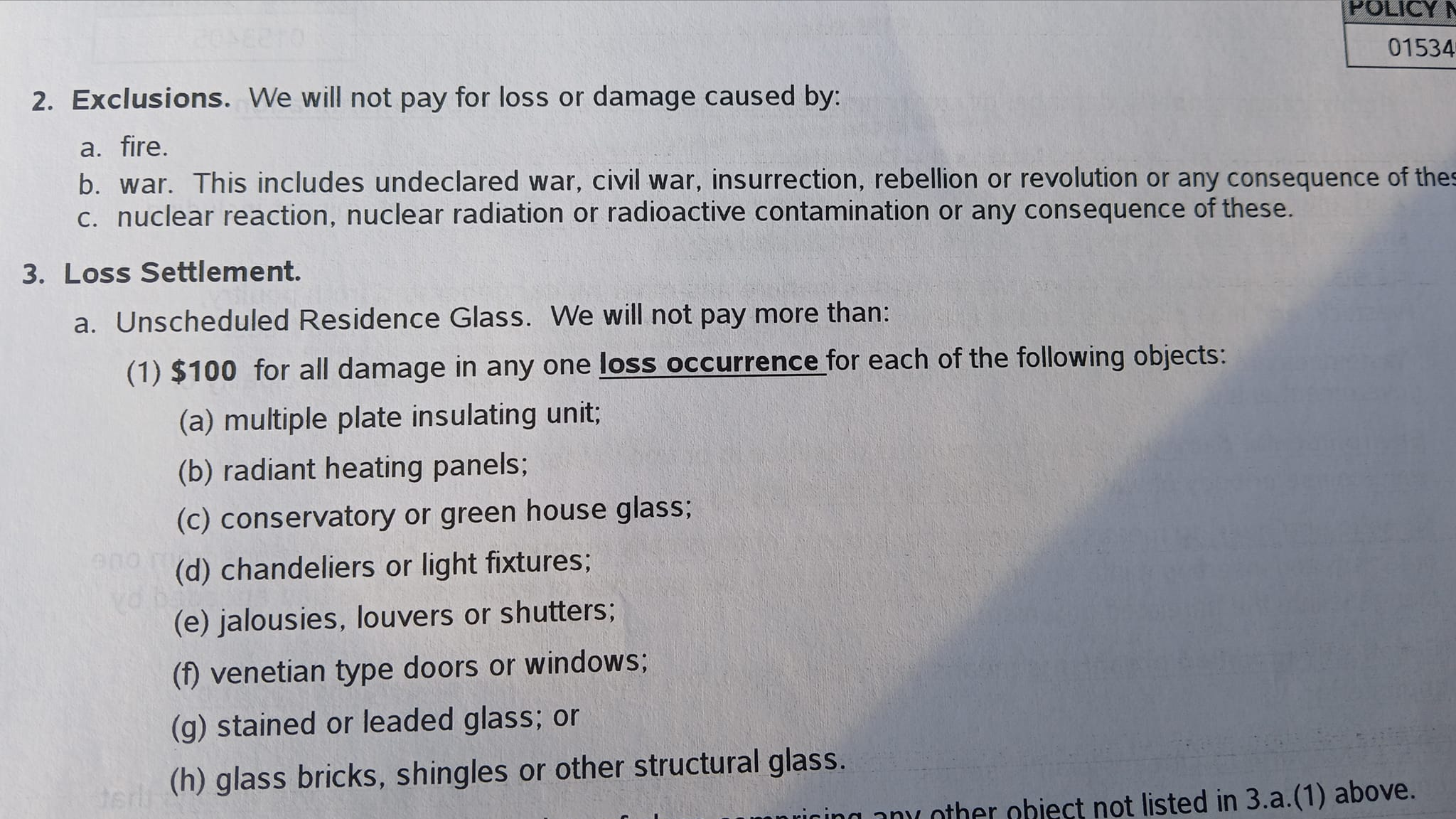

Exclusion 2a: Fire

This may seem obvious, but it's not always covered under homeowner's insurance. It can refer to natural disasters like wildfires, and if the entire area was affected, then your policy wouldn't cover any damage to your home. -

Exclusion 2b: War.

Now this is a bit of a surprise. This includes undeclared war, civil war, insurrection, rebellion or revolution, or any consequence of these. It's clear that they're not just talking about international conflicts here - they're also considering domestic unrest. -

Exclusion 2c: Nuclear reaction, nuclear radiation, radioactive contamination or any consequence of these

Again, this isn't something you'd expect to find in a homeowner's insurance policy. But it does raise some interesting questions about what companies might know that we don't.

What These Changes Mean

Now let's look at why these exclusions might be relevant:

- Fire: This could cover natural disasters, economic collapse leading to widespread destruction or even intentional arson.

- War: Given the world's current political climate and increasing domestic unrest in many countries, it would make sense for insurance companies to start considering this as a potential risk.

- Nuclear reactions: There are concerns about nuclear power plants around the world, and what happens if there was an accident.

Theories About What Insurance Companies Know

It's important to note that these exclusions don't mean that any of these events will definitely happen - but they do indicate that insurance companies are at least considering them as possibilities.

This raises some interesting questions about what else insurance companies might know that we don't. They have access to a lot of data from various sources, including government, academia, and private research institutions. It's possible they've been given information that the general public isn't aware of yet.

Conclusion

The changes in these policies suggest that something is being considered by insurance companies that might not have been on their radar before. They're preparing for potential outcomes that could impact our homes, our lives - and perhaps even the very survival of America itself.

This doesn't mean we should panic or believe in some grand conspiracy theory. But it does remind us to keep an eye out for signs around us, to stay informed, and most importantly, to take steps to prepare ourselves and our families for potential disasters.